Categories

Tags

-

#Aerospace 3D Printing Market Share

#Plant Growth Chambers Market Share

#Nurse Call Systems Market Size

#Cosmetic Dentistry Market Size & Share

#Plant Growth Chambers Market Size

#Packaged Coconut Water Market Share

#Heparin Market Size

#Burn Care Market share

#3D Printing Market Size

#3D Printing Market Trends

#Cosmetics Market Size

#Cosmetics Market Share

#Cosmetics Market Trends

#Anti-Money Laundering (AML) Software Market

#Chemoinformatics Market Size

#Global Eggshell Membrane Market Size

#Audio DSP Market Share

#Pasta Sauce Market share

#Medical Tourism Market Size

#Offshore Support Vessels Industry Overview

#Workwear Market Size

#Autoinjector Market Size

#Autoinjector Market Share

#Autoinjector Market Trends

#Pharmaceutical Filtration Market Share

#Wallpaper Market Share

#South Korea API Market Outlook: Digital Integration

#South Korea Forage Market Size

#South Korea Forage Market share

#South Korea Forage Market Trends

#Battery Electrolyte Market Size

#South Korea Advertising Market Outlook

#South Korea Advertising Market share

#South Korea Advertising Market growth

#Plant Growth Chambers Market Trends

#Cosmetic Dentistry Market 2025: Size

#Cosmetic Dentistry Market Trends

#Rhinoplasty Market share

#Rhinoplasty Market size

#Rhinoplasty Market Trends

#Dietary Fiber Market Size

#South Korea Drones Market Report

#South Korea Drones Market share

#South Korea Drones Market Trends

#Marine Plywood Market Size

#Marine Plywood Market Share

#Marine Plywood Market Trends

#Structural Core Materials Market Size

#Recommendation Engine Market Share

#Coconut Water Market Size

#Coconut Water Market Trends

#South Korea Electric Vehicle Market share

#South Korea Electric Vehicle Market Report 2025–2033: Size

#South Korea Electric Vehicle Market Trends

#Microgreens Market Size

#Microgreens Market Share

#Microgreens Market Trends

#Global Mezcal Market Size

#Cotton Yarn Market Size

#Global Virtual Data Room Market share

#Global Virtual Data Room Market size

#Global Virtual Data Room Market Trends

#Sustainable Athleisure Market Size

#Sustainable Athleisure Market share

#Sustainable Athleisure Market Trends

#Coffee Roaster Market Analysis

#Coffee Roaster Market share

#Coffee Roaster Market size

#High-End Lighting Market share

#High-End Lighting Market Size

#High-End Lighting Market Trends

#Fire Alarm and Detection System Market Size

#Fire Alarm and Detection System Market share

#Fire Alarm and Detection System Market Trends

#Lung Cancer Therapeutics Market Size

#Lung Cancer Therapeutics Market share

#Lung Cancer Therapeutics Market Trends

#3D printing materials market Size

#3D printing materials market share

#3D printing materials market Trends

#Cashew Milk Market Size

#Cashew Milk Market share

#Cashew Milk Market Trends

#jewellery market share

#jewellery market size

#jewellery market Trends

#Energy Drinks Market share

#Energy Drinks Market size

#Energy Drinks Market Trends

Archives

Structural Core Materials Market Size, Growth, Key Players, Tre

-

IMARC Group, a leading market research company, has recently released a report titled "Structural Core Materials Market Size, Share, Trends and Forecast by Product Material, Skin Material, End Use, and Region, 2025-2033." The study provides a detailed analysis of the industry, including the global structural core materials market Trends, share, size, growth and forecast. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

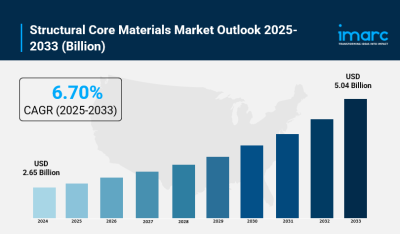

The global structural core materials market was valued at USD 2.65 billion in 2024. It is projected to grow to USD 5.04 billion by 2033, expanding at a CAGR of 6.70% during the forecast period 2025–2033. The market growth is driven by strong demand in aerospace, automotive, wind energy, and construction sectors, fueled by advancements in composite technologies and increasing focus on sustainability.

STUDY ASSUMPTION YEARS

- Base Year: 2024

- Historical Years: 2019-2024

- Forecast Period: 2025-2033

STRUCTURAL CORE MATERIALS MARKET KEY TAKEAWAYS

- Current Market Size: USD 2.65 Billion in 2024

- CAGR: 6.70%

- Forecast Period: 2025-2033

- North America dominates with a market share of over 35.6% in 2024, driven by aerospace, automotive, and wind energy industries.

- Honeycomb cores lead the product segment with a 63.5% market share in 2024.

- Carbon Fiber Reinforced Polymer (CFRP) is the leading skin material due to its strength and weight benefits.

- Aerospace is the largest end-use segment with 38.1% share, owing to demand for lightweight materials enhancing fuel efficiency.

- Technological advancements such as automation and 3D printing are accelerating market growth.

Claim Your Free “Structural Core Materials Market” Insights Sample PDF: https://www.imarcgroup.com/structural-core-materials-market/requestsample

MARKET GROWTH FACTORS

The demand of structural core materials is expected to increase during the forecast period as usage of lightweight materials in aerospace, wind energy, automotive and construction industries is expected to increase due to their ability to provide higher fuel efficiency and lower carbon emissions. Wind energy has also used the strength-weight ratio of the material in turbine designs which use longer blades to increase efficiency, and automotive applications have become more common, for electric vehicles with increased crashworthiness despite reduced weight. Durability and the advent of sustainable composite technologies have increased their potential applications.

Growing environmental concerns have resulted in the development of eco-friendly core materials in keeping with global sustainability initiatives. R&D investments for developing new materials are likely to increase market growth. In November 2024 for example, 3A Composites Core Materials introduced the Engicore business line, which provides tailor-made, custom-shaped cores to suit manufacturing and sustainability requirements; ensuring a strong global demand and sufficient growth.

Automated fiber placement, vacuum infusion, and 3D printing are new technologies. They improve composite performance. They reduce costs. They offer lower waste and weight. New resin systems and reinforcements improve the durability of core materials for use in harsh environments. Smart technology embeds sensors into resin to monitor and predict maintenance in high-performance applications, including automotive, marine, aerospace, and renewable energy sectors, which leads to growing demand in these fields.

Several environmental factors influence the structural core materials market, for manufacturers focusing on biodegradable and recyclable materials to comply with regulations and sustainability initiatives. An example of this is the April 2023 launch of the first sustainable core materials using reprocessed PET. Their insulation performance, low resin absorbency, and light overall weight efficiency provide energy savings within the aerospace, automotive, and construction fields. Sustainable materials, including bio-based resin and renewable fibers, can grow the future market as research and development receive funding.

MARKET SEGMENTATION

Breakup By Product Material:

- Foam: Not provided in detail, generally used for lightweight structural applications.

- Balsa: Not provided in detail, a natural wood core material with good strength-to-weight ratio.

- Honeycomb: Dominates the market with 63.5% share in 2024. Known for excellent strength-to-weight ratio and energy absorption, used broadly in aerospace, automotive, and marine industries. Lightweight nature reduces fuel consumption and enhances performance.

Breakup By Skin Material:

- Glass Fiber Reinforced Polymer (GFRP): Not detailed in description.

- Carbon Fiber Reinforced Polymer (CFRP): Leading skin material valued for exceptional strength, stiffness, and low weight. Used in aerospace, automobile, and renewable energy for improved performance and corrosion resistance.

- Nylon Fiber Reinforced Polymer (NFRP): Not detailed in description.

- Others: Not detailed in description.

Breakup By End Use:

- Aerospace: Largest end-use segment with 38.1% market share in 2024. Demand driven by need for lightweight, strong materials that save fuel consumption in aircraft wings, fuselages, and interiors.

- Automotive: Growing use in electric vehicles and other automotive applications for reduced weight and enhanced safety.

- Wind Energy: Structural core materials used to construct durable and efficient turbine blades.

- Marine: Not detailed in description.

- Construction: Increasing due to demand for durable and sustainable composite technologies.

- Others: Not detailed.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America leads the global structural core materials market with a 35.6% share in 2024. The region sees strong demand in aerospace, automotive, and wind energy sectors. As a prime aerospace manufacturing hub, advanced structural materials meet high performance and fuel efficiency standards. The growth in electric vehicles and renewable energy projects further supports market expansion. Additionally, technological advancements and sustainability initiatives consolidate North America's dominant position in the industry.

RECENT DEVELOPMENTS & NEWS

In September 2024, Armacell launched ArmaFlex® ECO550 adhesives that improve efficiency, safety, and sustainability in insulation applications by requiring only one-third the quantity of conventional adhesives. This solvent-free product complies with LEED® and BREEAM® certifications. In November 2024, Evonik unveiled PA12-based INFINAM® 6013 P and 6014 P powders featuring carbon black for enhanced UV resistance and durability at Formnext 2024. Evonik also presented HP 3D HR PA12 FR, a halogen-free, flame-retardant polymer with 50% reusability, enhancing sustainable 3D printing for aerospace, automotive, and electronics industries.

KEY PLAYERS

- Armacell

- Diab Group

- Euro-Composites

- Evonik Industries AG

- Gurit Services AG

- Schweiter Technologies AG

- The Gill Corporation

Ask Analyst For Request Customization: https://www.imarcgroup.com/request?type=report&id=27628&flag=E

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

ABOUT US

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:

+91 120 433 0800

+91 120 433 0800United States: +1-201971-6302